In the realm of cashless payments, acquiring, or payment by bank card, stands out as one of the most convenient methods. This mode of transaction is seamlessly integrated into a myriad of retail establishments, ranging from quaint kiosks to expansive stores. Today, we delve into the intricacies of acquiring, exploring how it functions in the Ukrainian landscape and unraveling its unique characteristics.

What is acquiring?

Acquiring is the process of accepting non-cash payments for goods and services using bank cards, both in physical retail outlets and online. The term itself comes from the English word “acquire,” which means “to receive.”

The main feature of acquiring is the automatic crediting of funds from the customer’s card directly to the entrepreneur’s current account, which distinguishes it from a standard bank transfer via IBAN.

Translated with DeepL.com (free version)

Statistics of non-cash transactions for 2024

According to the National Bank of Ukraine, in 2024, the number of non-cash transactions in Ukraine increased to 94.6% of the total number of transactions. Ukrainians actively paid with cards both in the country and abroad, making more than 8 billion non-cash payments worth UAH 4.2 trillion.

This growth demonstrates that Ukraine’s payment infrastructure is stable and uninterrupted, and that people’s confidence in cashless payments continues to grow.

The popularity of contactless cards is also growing – in December 2024, their number reached 35 million, which is 14% more than in 2023. More than 60% of all active cards now support contactless payments.

The use of tokenized cards (NFC) is growing even faster. Their number increased by 33% to 16.5 million.

How acquiring works?

At its core, payment by acquiring is a multilateral process, involving key participants:

- Buyer — initiates payment using a bank card.

- Seller — accepts payments through a POS terminal.

- Acquiring Bank — provides and maintains the POS terminal, processes payments, and offers technical support.

- Issuing Bank — issues the card, verifying the account balance for payment authorization.

To receive payments from bank cards, the seller enters into an agreement with the acquiring bank and installs a POS terminal at the point of sale. Payment through the terminal is as follows:

- the buyer attaches or inserts a bank card to the POS terminal;

- the terminal reads the card data and sends a request to the issuing bank to check the card balance;

- after verification, the issuing bank confirms the payment (or, in case of fraud, cancels it and blocks the card);

- the POS terminal issues a receipt to the customer.

With a stable internet connection, the entire transaction transpires within a matter of seconds. The bank debits the payment amount from the card and transfers it to the seller’s account after a certain period of time. The transfer period is specified in the contract.

Types of acquiring

Different industries leverage distinct technical tools for bank card transactions. Here are three prominent types:

Internet acquiring

Ideal for Online Commerce: Predominantly used in online transactions, buyers make payments through secure web interfaces. To avoid fraud, the seller must create a secure infrastructure for making payments. Therefore, internet acquiring is often facilitated by third-party providers.

Merchant acquiring

Retail’s Go-To: widely adopted in retail settings such as shops and supermarkets, buyers leverage POS terminals connected to cash registrars.

Both push-button and Android touchscreen POS terminals are used at points of sale. Payment methods vary from contact (the customer inserts the card into the terminal) to contactless (when the customer taps the card into an NFC device), and even virtual cards on smartphones.

Mobile acquiring

On-the-Go Convenience: Suited for services like taxis and couriers, this method allows sellers to accept payments via smartphones or tablets, offering unparalleled mobility. Installation of a specialized program is all that’s required.

Mobile acquiring technologies

Mobile acquiring in Ukraine embraces versatile technologies, including the following.

QR acquiring

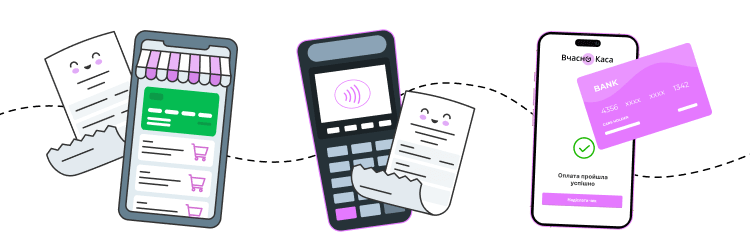

The seller creates a QR code for the goods in the program. The customer scans the code and goes to the payment page, enters bank card details, or uses Apple Pay or Google Pay. After payment, the seller issues a fiscal receipt to the customer.

Tap to Phone

With Tap to Phone technology, merchants use a smartphone as a POS terminal without additional equipment. In the banking app or cash registrar app, the amount of payment is shown, and the customer taps a bank card or a virtual card to the smartphone. The data is read by the module and the funds are transferred to the merchant’s account. The customer then receives an electronic fiscal receipt.

What terminal should a sole proprietor choose for a cash registrar?

Acquiring in trade is used not only by legal entities but also by individual entrepreneurs. After all, according to the current Ukrainian legislation, from January 1, 2024, all points of sale in settlements with 5000 or more inhabitants must provide the possibility of cashless payments.

When choosing between POS terminals and mobile acquiring technologies, you should consider the following factors.

Type of activity. Mobile acquiring is the best solution for courier, transportation services, or home-based equipment repair. In shops and coffee shops, it is more convenient to use POS terminals.

Economic feasibility. The POS terminal issues 2 receipts – for the buyer and the seller. They may be needed to prove the fact of payment in cases where the funds have not been credited to the seller’s account. At the same time, mobile acquiring (QR, Tap to Phone) does not require funds for terminal maintenance, rent, etc. Therefore, when choosing an acquiring technology for your cash desk, evaluate the advantages of each and the costs associated with them.

Payment of the commission. This is important from the point of view of taxation of individual entrepreneurs. The acquirer can charge a commission for its services for each transaction before the funds are credited to the sole proprietor’s account or withdraw a fixed amount from the account every month.

Moreover, it is important to consider the technical capabilities of connecting acquiring to the cash registrar. In particular, any model of the terminal can be connected to Vchasno.Kasa. First of all, find out what protocol the acquiring bank uses. You can use Device Manager to connect the terminal to Vchasno.Kasa. Install the program for managing the cash registrar and the terminal on the cashier’s computer and add the bank terminal.

Why should businesses connect acquiring?

Choosing a reliable acquiring bank gives a business a significant competitive advantage, improves its reputation, increases customer confidence, and contributes to profit growth.

However, acquiring is also about the security and convenience of payment processing. It opens up new opportunities for business development, increases revenue, and optimizes processes.

Key benefits of the solution:

✔︎ Increased sales. The absence of restrictions on payment methods motivates customers to make purchases more often and for larger amounts. Statistics confirm that the average receipt for non-cash payments is higher than for cash payments.

✔︎ Convenience for customers. Modern customers prefer contactless payments, so the ability to pay with a card or smartphone increases trust in the company and creates a positive customer experience.

✔︎ Speed of service. Sellers don’t need to spend time counting cash and issuing change, which significantly speeds up the purchase process.

Financial security. Acquiring minimizes the risks associated with fraud, counterfeiting, and theft. Each transaction is checked in the banking system, which makes it impossible to carry out any fraud with cash.

✔︎ Staff efficiency. The cashier no longer needs to spend time counting money and issuing change, which significantly speeds up his work and reduces the likelihood of errors.

✔︎ Analytics. Connecting acquiring gives you access to detailed sales statistics, which allows you to better understand customer behavior and preferences. You will be able to analyze the average check, the frequency of purchases, popular goods or services, as well as seasonal fluctuations in demand.

In addition, non-cash payments are automatically recorded in the system, which simplifies accounting, reduces the risk of errors, and promotes transparency of payment transactions.

The only caveat is the cost of acquiring. Business owners need to take into account the cost of equipment, a stable Internet connection, and fees for each transaction. However, the benefits of cashless payments often far outweigh these costs.

Easily and quickly connect any acquiring to Vchasno.Kasa

and fiscalize payments.

Integration with over 12 banks in Ukraine